US ESG Regulatory Reporting: Comprehensive Requirements and Implementation Phases

US ESG Regulatory Reporting Requirements:

The SEC unveiled a landmark proposal for companies to disclose a wide variety of data on their climate-related risks (and opportunities). The proposed rule includes already well disclosed metrics (Scope 1 & 2 GHG emissions), more expansive, less widely-reported Scope 3 emissions (only where material or where companies already have set an emissions target incorporating Scope 3), as well as some qualitative disclosures similar to those codified by the Task Force on Climate-Related Financial Disclosures (TCFD), exceeding our expectations of a more modest Scope 1 & 2-focused framework.

Presentation and Attestation of the Proposed Disclosures:

The proposed rules would require a registrant (including a foreign private issuer) to:

- Provide the climate-related disclosure in its registration statements and Exchange Act annual reports, for example on Form 10-K;

- Provide the Regulation S-K mandated climate-related disclosure in a separate, appropriately captioned section of its registration statement or annual report;

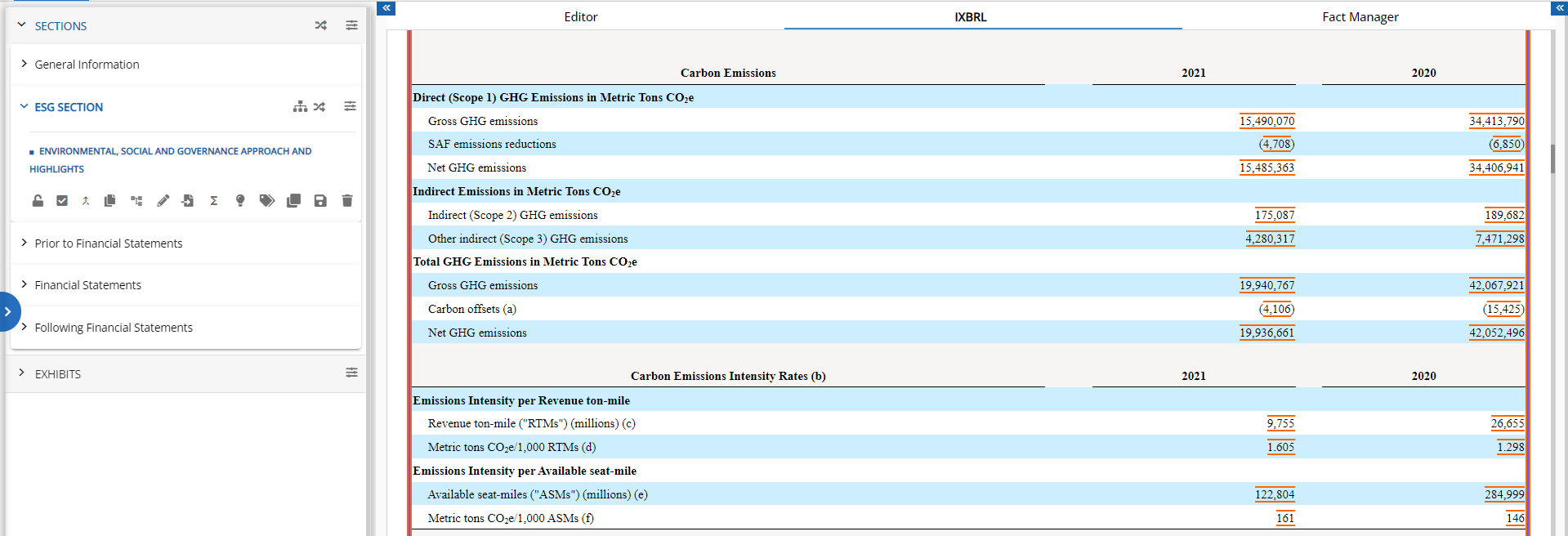

- Provide the Regulation S-X mandated climate-related financial statement metrics and related disclosure in a note to its consolidated financial statements;

- Electronically tag both narrative and quantitative climate-related disclosures in Inline XBRL; and

- If an accelerated or large accelerated filer, obtain an attestation report from an independent attestation service provider covering, at a minimum, Scopes 1 and 2 emissions disclosure.

Phase-In Periods and Accommodations for the Proposed Disclosures

The following tables assume that the proposed rules will be adopted with an effective date in December 2022 and that the filer has a December 31st fiscal year-end:

| Registrant Type | Disclosure Compliance Date | |

|---|---|---|

| All proposed disclosures, including HG emissions metrics: Scope 1, Scope 2, and associated intensity metric, but excluding Scope 3 | GHG emissions metrics: Scope 3 and associated intensity metric | |

| Large Accelerated Filer | Fiscal year 2023 (filed in 2024) | Fiscal year 2024 (filed in 2025) |

| Accelerated Filer and Non-Accelerated Filer | Fiscal year 2024 (filed in 2025) | Fiscal year 2025 (filed in 2026) |

| SRC | Fiscal year 2025 (filed in 2026) | Exempted |

| Filer Type | Scopes 1 and 2 GHG Disclosure Compliance Date | Limited Assurance | Reasonable Assurance |

|---|---|---|---|

| Large Accelerated Filer | Fiscal year 2023 (filed in 2024) | Fiscal year 2024 (filed in 2025) | Fiscal year 2026 (filed in 2027) |

| Accelerated Filer | Fiscal year 2024 (filed in 2025) | Fiscal year 2025 (filed in 2026) | Fiscal year 2027 (filed in 2028) |

SEC recently mandated the Climate disclosure:

- Greenhouse gas emissions disclosures

- Climate-related risks

- Aligns with TCFD framework

Our SAAS based disclosure management platform allows:

- Preparation of regulatory reports

- Automates the generation of XBRL

- Ensures accuracy and compliance

XOR a multi-user cloud-based online XBRL review platform allows:

- Review of ixbrl filings.

- Built-in validation reports

- Workflow management capabilities.

{kind=link}