If your organisation is navigating sustainability reporting obligations in Europe, 2026 is a pivotal transition year. Over the past two years, EU sustainability regulations — especially the Corporate Sustainability Reporting Directive (CSRD) and the EU Taxonomy Regulation — have evolved, with major updates that will shape your reporting obligations, data systems, and stakeholder disclosures.

Rather than waiting until the last minute, you need to build momentum now — strengthening your data governance, aligning your reporting processes, and preparing for integrated sustainability disclosures that meet both CSRD and EU Taxonomy expectations.

1. What Happened in 2024–2025 That Shapes 2026 Reporting

a) CSRD First Reporting Waves Began in 2024–2025

- The CSRD officially entered into force in 2023, and reporting for companies already under the earlier NFRD began with the 2024 financial year, with publications due in 2025.

- From 2025 onward, CSRD expanded to cover more large companies, requiring them to prepare detailed sustainability disclosures using the European Sustainability Reporting Standards (ESRS).

These early waves mean that many organisations have already had to establish foundational reporting practices — governance structures, data collection systems, and internal review processes. If you have started reporting already, you are ahead; if not, 2026 is your window to catch up.

b) Omnibus and “Stop-the-Clock” Changes

During 2025, EU legislators introduced the Omnibus simplification package and a Stop-the-Clock directive that revised CSRD’s scope and timelines:

- The directive postponed compliance for many companies originally scheduled to report in 2026 — particularly those not in the first wave — to later years (e.g., 2027 or beyond).

- Thresholds for coverage were also recalibrated in some proposals so that only companies with more than 1,000 employees and €450 million turnover are mandatorily covered in early implementation.

These legislative updates do not eliminate reporting obligations — they give you time to prepare with greater clarity and structure than before.

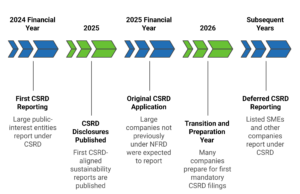

2. CSRD Timeline: What You Need to Know for 2026

CSRD implementation follows a phased approach, but recent regulatory developments — including the Omnibus simplification package and the “Stop-the-Clock” directive — mean that 2026 functions less as a first-time reporting year and more as a structured preparation and transition year for many organisations.

Companies Already Reporting Under CSRD (Former NFRD Entities)

Large public-interest entities previously subject to the Non-Financial Reporting Directive (NFRD) that completed their first CSRD-aligned sustainability reporting for the 2024 financial year, with disclosures published in 2025.

Large Companies Newly in Scope of CSRD

Large EU companies that were not previously covered by NFRD and meet at least two of the following EU size criteria:

- More than 250 employees

- Net turnover exceeding €50 million

- Total assets exceeding €25 million

Under the original CSRD timetable, these companies were expected to report for the 2025 financial year. However, following the EU’s “stop-the-clock” and simplification measures, the initial application of CSRD for many companies in this category has been postponed, subject to national transposition and final scope determinations.

As a result, 2026 is widely viewed as a transition and preparation year, with organisations strengthening data foundations and reporting processes ahead of first mandatory filings.

Listed SMEs and Other Companies with Deferred CSRD Start Dates

Listed small and medium-sized enterprises that meet the EU SME definition:

- Fewer than 250 employees, and

- Either net turnover of €50 million or less or total assets of €43 million or less

These companies generally fall into later CSRD reporting phases and benefit from deferred application timelines and transitional provisions, with mandatory reporting expected in subsequent years following further EU and national clarification. Many are using earlier years to prepare internally.

What this means for you:

Regardless of which category applies, 2026 remains an important year to strengthen data governance, complete ESG data mapping, and test audit-ready disclosure processes aligned with ESRS — even where mandatory reporting dates have been deferred.

3. Why EU Taxonomy Matters for 2026 Reporting

The EU Taxonomy Regulation provides a classification system for environmentally sustainable economic activities. While this regulation has existed alongside sustainability reporting frameworks for several years, its role is becoming more important in your 2026 disclosures for two key reasons:

- Taxonomy alignment affects how you describe sustainable activities in your CSRD reports — especially climate, water, circular economy, and pollution prevention contributions.

- Taxonomy screening criteria and “do no significant harm” principles are currently being reviewed and may evolve in 2026, offering new guidance on practical compliance.

Rather than treating Taxonomy reporting separately, you should be integrating it into your broader ESG reporting processes now — mapping which economic activities qualify and how your sustainability data supports those classifications.

4. Four Practical Steps You Must Take Now

To prepare effectively for your 2026 reporting obligations, here’s what you should be doing today:

Step 1: Strengthen Your Data Governance

Identify where sustainability-related data currently resides, who owns it, and how it flows into reporting processes. Create clear roles and responsibilities for CSRD and Taxonomy data owners.

Step 2: Build Integrated Reporting Processes

Instead of creating separate structures for CSRD and Taxonomy, integrate reporting workflows — so one reliable data pipeline feeds both sets of disclosures.

Step 3: Prepare for Assurance and Audit-Readiness

CSRD reporting is expected to be subject to assurance requirements (initially limited assurance) — meaning data must be traceable, defensible, and stored with proper controls.

Step 4: Monitor Evolving Requirements

The EU continues to refine CSRD standards, Taxonomy criteria, and other related sustainable finance rules. Keep tracking updates from EU institutions and adapt your processes early — rather than reacting later.

How EcoActive Helps You Stay CSRD-Ready

EcoActive supports you as you prepare for CSRD by helping you manage sustainability data, align disclosures with ESRS, and maintain consistency as reporting expectations evolve.

With EcoActive, you can:

- Manage ESG data comprehensively

Centralise sustainability and related financial data to support structured, CSRD-aligned reporting. - Apply strategic analytics to your disclosures

Analyse ESG data to better understand trends, gaps, and priorities across CSRD requirements. - Stay aligned with evolving CSRD and ESRS requirements

Work with up-to-date regulatory structures that reflect current EU sustainability standards. - Streamline CSRD reporting processes

Reduce manual effort through guided workflows that support efficient data collection and disclosure preparation. - Prepare XBRL-ready sustainability outputs

Generate structured data suitable for digital and regulatory reporting as CSRD requirements mature. - Work from an integrated ESG and financial reporting platform

Align sustainability information with financial data to improve consistency across disclosures. - Calculate GHG emissions within the platform

Measure Scope 1, Scope 2, and relevant Scope 3 emissions to support climate-related CSRD disclosures. - Use Agentic AI to support workflows and reporting

Apply Agentic AI to assist with drafting, validation, and coordination across reporting teams. - Benchmark your disclosures against peers

Compare material topics and performance across industry groups to inform CSRD-aligned reporting decisions.

Conclusion

Even though regulatory timelines have been updated and some reporting dates extended, 2026 is a year for structured preparation — ensuring your data governance, integrated reporting processes, and audit-ready output are resilient and aligned with evolving EU expectations.

By acting now, you position your company not just to comply, but to provide sustainability disclosures that inspire trust, improve investor confidence, and support strategic decision-making across your business.

Explore how EcoActive can support your CSRD preparation for 2026 and beyond.

Build a connected, audit-ready sustainability reporting foundation that evolves with EU requirements. Book a Demo