Annual Report Season Tends to Look Similar Across Organisations

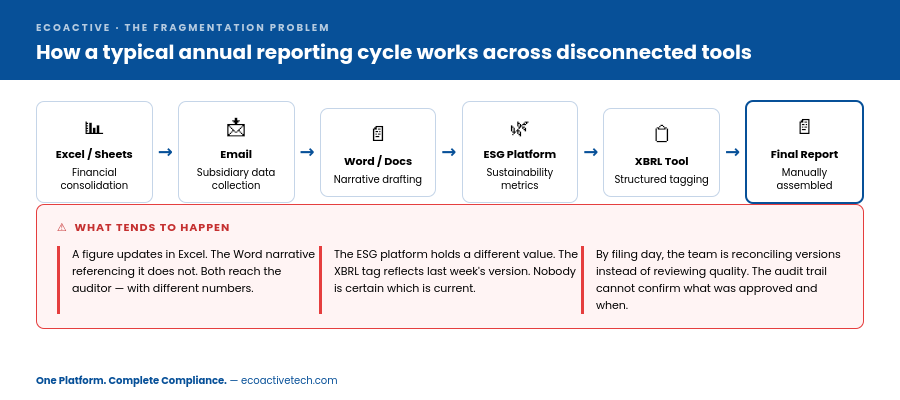

Many reporting teams managing the annual report cycle find themselves working across a dozen or more active files. The IFRS financial statements sit in one system. The narrative sections live in a separate Word document. ESG metrics are tracked in another platform. The XBRL tags are managed in yet another tool — sometimes by a different team entirely. And somewhere in the mix, there is usually a shared drive of spreadsheets that nobody is entirely confident in.

This is a common pattern, not a sign of poor management. It reflects the fact that financial reporting and sustainability reporting developed separately over many years, each gaining its own tools and processes, before the regulatory environment began requiring them to appear in the same document.

The challenge becomes most visible when something changes — a revised figure, an updated metric, a late-stage review comment — and teams have to trace that change manually across every system and document it touches. That is where the coordination overhead tends to show up.

Spreadsheet-Based Workflows Remain Widespread in Finance

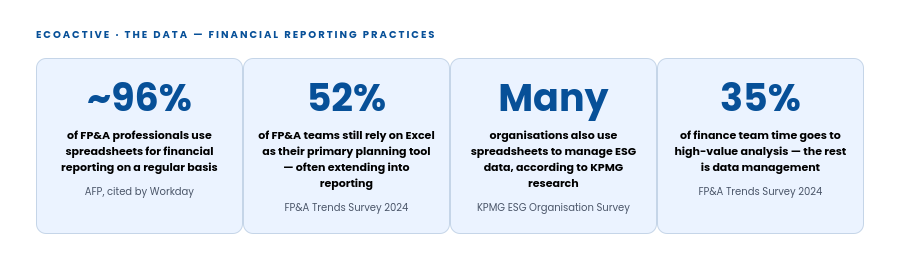

Research into financial reporting practices consistently finds that spreadsheet-based workflows remain common even in large, well-resourced finance functions — often persisting alongside more recent ESG and ERP investments.

A dedicated ESG platform or ERP system does not always eliminate spreadsheet use — they tend to remain at the handoff points between systems, where data moves from one tool to the next.

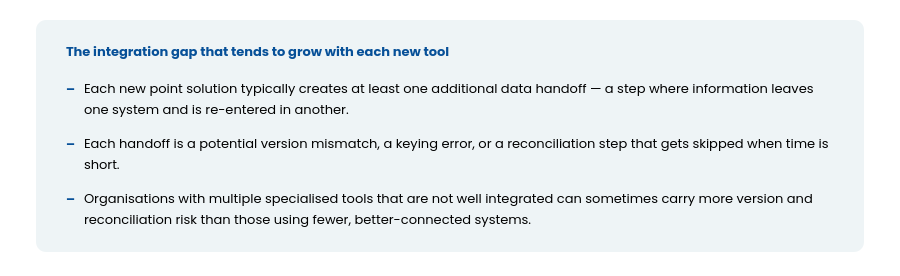

Tools tend to accumulate over time. Integration between them often does not keep the same pace.

In short:

Spreadsheet reliance in financial reporting reflects the real flexibility and familiarity that finance teams find valuable. The question it raises is what happens when those spreadsheets are part of a workflow that also needs to produce a consistent, audit-ready, filed disclosure.

Where the Annual Reporting Cycle Gets Complicated

Fragmented workflows rarely break down with a clear, visible error early in the process. They tend to produce small inconsistencies that accumulate over the cycle and become time-consuming to resolve close to the deadline. Finance teams across sectors and sizes tend to recognise the same patterns.

Keeping financial narrative and supporting numbers consistent throughout

Annual reports prepared under IFRS, SEC filing requirements, or ESEF mandate consistency between the financial statements and the narrative sections of the document. A revenue figure cited in the management commentary should match the one in the accounts. A climate-related risk quantification in the strategic report where applicable, reflected consistently in the structured (iXBRL) output.

In a fragmented workflow, that consistency is maintained manually — usually close to the filing date, by people managing multiple priorities at once. A disclosure that is individually accurate in each section can still carry inconsistencies across the document, which may lead to audit findings or, in some cases, post-filing corrections.

A familiar scenario: a revenue or cost figure changes late in the review process. Three sections of the report reference it. Two get updated. One does not. The inconsistency reaches the external auditor.

ESG data entering a financial reporting workflow

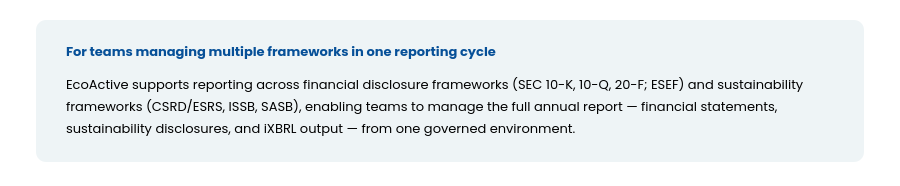

One of the more recent sources of complexity for finance teams is the integration of ESG data into documents that have historically been purely financial. Under CSRD, for in-scope EU entities, sustainability disclosures must appear within the management report. Under ESEF, listed EU issuers already tag IFRS consolidated financial statements in Inline XBRL. Separately, digital tagging of sustainability disclosures is developing through the CSRD/ESRS digital reporting architecture. In jurisdictions adopting ISSB-aligned requirements, sustainability-related financial disclosures are increasingly expected to align with financial reporting timelines, governance processes, and investor-focused materiality.

This creates a practical workflow question that goes beyond data availability: how do two previously separate processes produce a single, consistent, governed document? There is no standard answer when those processes run in disconnected systems.

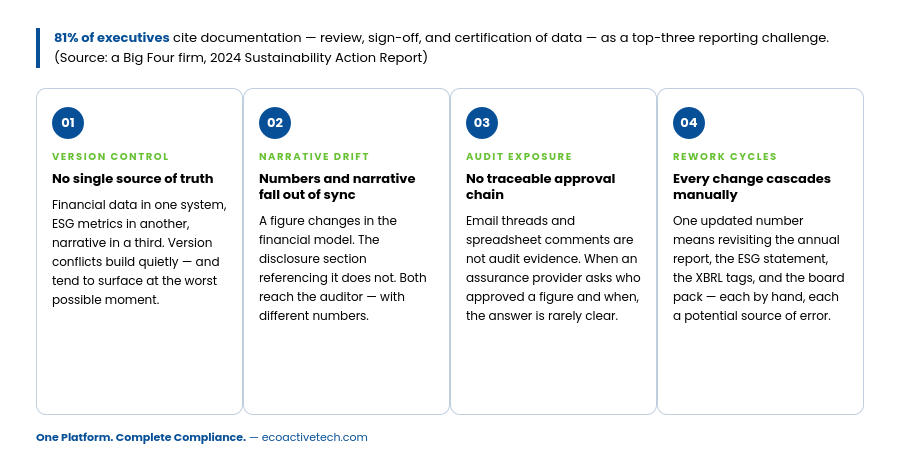

The audit trail question

Approximately 81% of executives cited documentation, review, and sign-off as a top-three reporting challenge, according to a Big Four firm’s 2024 Sustainability Action Report. Assurance over ESG disclosures, now required or expected under CSRD for applicable companies, and increasingly expected in jurisdictions adopting ISSB-aligned frameworks, calls for the same quality of evidence as financial audit. Email sign-offs and versioned spreadsheet filenames are increasingly insufficient as the primary record.

In short: The audit trail question is not new to finance — most teams are familiar with the difficulty of reconstructing an approval chain for a financial figure under auditor scrutiny. Adding ESG into the same report extends that challenge to data that typically has fewer established controls and a shorter history of formal governance. → See how EcoActive connects financial and ESG reporting workflows |

Why Adding Tools Has Not Always Solved the Problem

When reporting requirements grow, the natural response is often to adopt a more specialized tool for the new requirement — a dedicated ESG data platform for sustainability metrics, a separate narrative editor for the annual report, and a standalone XBRL tool for structured tagging. Each addresses a specific gap. Each also introduces a new handoff point between systems.

The regulatory direction across major frameworks is moving toward convergence: ESG disclosures are increasingly required inside the financial report, not alongside it. Under CSRD (for in-scope EU entities), the sustainability statement is part of the management report. Under ESEF, financial statements are mandatorily tagged in Inline XBRL, with ESG tagging requirements developing under CSRD/ESRS. Under ISSB in jurisdictions where standards are adopted or under consideration, climate disclosures are intended to align with financial reporting timelines. Treating these as entirely separate workstreams tends to increase the coordination burden with each new mandate.

In short:

Spreadsheet reliance in financial reporting reflects the real flexibility and familiarity that finance teams find valuable. The question it raises is what happens when those spreadsheets are part of a workflow that also needs to produce a consistent, audit-ready, filed disclosure

→ Explore how EcoActive supports multi-framework financial and ESG reporting

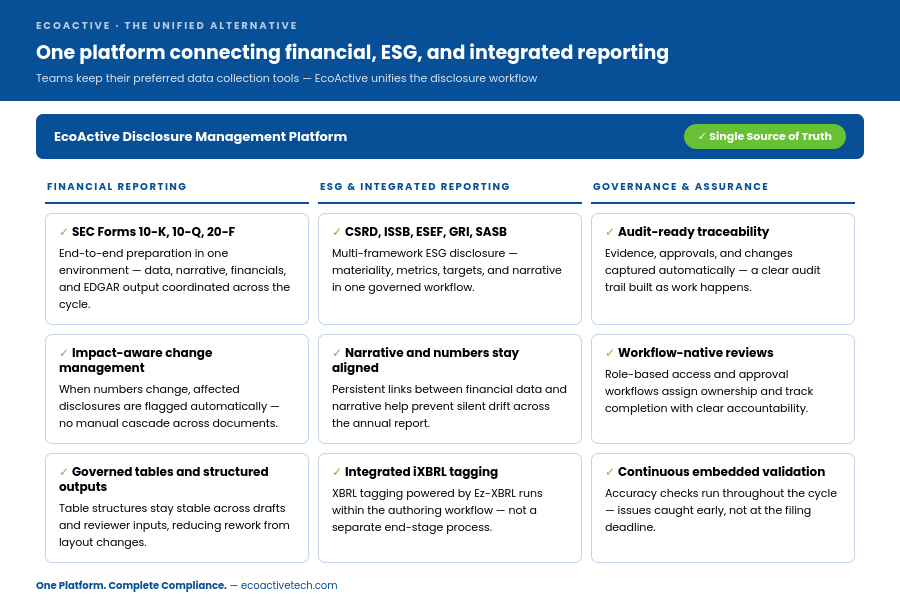

What Connecting Financial and ESG Reporting Can Look Like

The goal for most finance teams is not to replace every tool in the workflow. ERP integrations, subsidiary collection templates, and third-party ESG data providers each serve a purpose that makes sense to maintain. The data collection layer can stay as it is.

What tends to benefit most from a unified approach is the disclosure workflow — the governed environment where collected financial and ESG data becomes narrative, receives approvals, gets tagged in XBRL, and is filed. That is where fragmentation creates the most practical risk, and where a connected environment has the most direct impact.

EcoActive is the layer where financial and ESG reporting connect — without requiring teams to replace the data collection tools they already rely on.

How the platform supports the annual reporting cycle

Underlying these capabilities is EcoActive’s agentic AI — which automates data population across the reporting cycle, surfaces prior-cycle disclosures to support continuity, and identifies emerging gaps before they reach review. The result is a workflow where teams spend less time constructing the report and more time governing it.

- Impact-aware change management: When a figure changes anywhere in the disclosure, the platform flags every section that references it — so review teams can address downstream effects without searching manually through the document.

- Narrative and financial data staying aligned: Persistent links between financial figures and narrative sections are designed to help maintain consistency across the annual report, significantly reducing the risk of narrative drift between review cycles.

- Governed tables and structured outputs: Table structures are maintained as governed objects across drafts and reviewer inputs — minimising the likelihood of layout changes creating rework or inconsistency.

- Integrated iXBRL tagging: XBRL tagging, powered by Ez-XBRL, is embedded within the authoring workflow rather than handled as a separate downstream step. Tags are applied as the document is built.

- Audit-ready traceability: Approvals, edits, and sign-offs are logged with timestamp and attribution as work progresses — building the audit trail continuously rather than reconstructing it under deadline pressure.

- Continuous embedded validation: Accuracy checks run throughout the reporting cycle, helping catch issues while there is still time to address them rather than at the point of filing.

The Overhead That Rarely Appears on a Budget Line

The operational cost of a fragmented reporting workflow rarely shows up as a line item. It appears instead as the hours spent reconciling spreadsheet versions the night before a filing deadline, as rework triggered when an inconsistency is found between the financial statements and a disclosure section, and as the compliance risk of a document that cannot demonstrate a clear, documented approval chain — which, in some cases, may lead to audit findings or post-filing corrections.

Research into corporate reporting practices consistently highlights that adapting reporting processes to meet new regulatory requirements is among the most significant operational challenges finance teams face — particularly when those processes depend on manual coordination between disconnected tools. The challenge is rarely a lack of understanding of the requirements. It tends to be the infrastructure needed to meet them consistently across the reporting cycle.

When that infrastructure relies on a collection of tools connected by manual handoffs, each new mandate introduces additional surface area for version mismatch, inconsistency, and audit exposure.

In short:

Fragmentation in reporting typically does not emerge from a deliberate choice — it tends to develop over time as teams adopt tools incrementally to meet growing requirements. Recognising it as a source of version risk, audit exposure, and deadline pressure is often the first step toward addressing it.

A Unified Platform Does Not Mean Less Control

Many finance teams approach the idea of a unified reporting platform with a reasonable concern: that consolidating onto a single environment means losing flexibility, or being locked into templates that do not fit how the team actually works.

EcoActive is built around the principle that teams should be able to collect data using whatever systems their organisation already uses. What the platform provides is the governed disclosure environment — where data that has been collected, in whatever format, becomes the reviewed, approved, and structured annual report. The collection layer stays as it is. The fragmentation in the disclosure layer is significantly reduced.

The number of frameworks, jurisdictions, and assurance requirements that sit inside the annual reporting cycle is growing, not contracting. The teams managing this complexity with the least pressure at deadline time tend to be the ones that addressed the disclosure infrastructure question earlier in the cycle.

Frequently Asked Questions

Q: What is fragmented reporting?

Fragmented reporting describes a situation where the financial data, ESG metrics, narrative content, and structured tagging needed to produce a single annual report are managed in separate, disconnected systems. Because these tools do not share data automatically, maintaining consistency across the document requires manual coordination — which introduces version risk and audit exposure at every handoff point.

Q: Why is producing a single annual report across financial and ESG frameworks complex?

Financial reporting and sustainability reporting developed separately, with their own tools, teams, and timelines. Regulatory convergence — CSRD placing sustainability disclosures inside the management report, ESEF requiring IFRS financial statements, and ISSB designing sustainability disclosure timelines to align with financial reporting in jurisdictions adopting or considering the standards — means those two workstreams increasingly need to produce a single, consistent, governed document. Most existing tool stacks were not built for that.

Q: What financial reporting tools do annual report teams typically rely on?

Most teams use a combination of ERP systems for source financial data, spreadsheets for consolidation and analysis, document editors for narrative drafting, ESG platforms for sustainability data, and XBRL tools for structured tagging. Research consistently shows spreadsheets remain in use at one or more stages even in large, listed organisations with dedicated reporting software.

Q: How do teams maintain an audit trail across financial and ESG disclosures?

An audit trail requires documentation of who approved what data, when, and on what basis — across both the financial and sustainability parts of the annual report. In fragmented workflows, this trail is typically reconstructed from email threads and file histories when required. Platforms that log edits, approvals, and sign-offs in real time as work progresses produce a continuous, available trail without the need for reconstruction at deadline.

Q: Does EcoActive replace the data collection tools a team already uses?

No. EcoActive is designed to connect to the source systems and collection tools a finance team already relies on — ERP integrations, subsidiary reporting templates, third-party ESG data providers. The platform manages the disclosure workflow: the governed environment where collected data is reviewed, approved, and produced as a filed, structured annual report. Teams retain their preferred collection tools.