Audit-Ready Financial and ESG Reporting Workflows: A Complete Guide

Audit-ready financial and ESG reporting workflows share the same fundamental problem: evidence assembled after the reporting cycle ends is inherently harder to validate and defend. Whether your auditor is reviewing an income statement adjustment or a GHG inventory, the question is the same — can you show where this number came from, who approved it, and what changed?

For finance teams, the risk is a late-stage revenue adjustment referenced in three sections of the annual report but updated in only two. For sustainability teams, it is a Scope 2 calculation whose utility invoices were never stored alongside the methodology. In both cases the answer to the auditor’s question requires the same scramble — reconstructing evidence that was never designed to be reconstructed.

This guide runs both challenges in parallel and shows how one workflow architecture resolves both.

What This Guide Covers

Organizations implementing audit-ready financial and ESG reporting workflows are better positioned to respond to growing audit, assurance, and compliance expectations.

Why financial and ESG audit evidence failures share the same root cause — and what that means for your workflow

How regulatory stakes are converging across financial audit standards, CSRD, ESEF, and ISSB

The four markers every disclosed figure must satisfy — applied to both financial and ESG data

Five pillars of a workflow that is audit-ready throughout the cycle, not just at year-end

How EcoActive captures traceability, approvals, and evidence for both financial and ESG in one governed platform

The Difference Audit Readiness Makes

| Without audit-ready workflows | With audit-ready workflows |

|---|---|

| Evidence assembled weeks after the close | Evidence captured as data is created |

| Financial and ESG managed in disconnected systems | One governed platform, one audit trail |

| Auditor queries delay reporting finalisation | Documentation available on demand |

| Assurance engagement cost is hard to predict | Strong evidence quality improves assurance efficiency and predictability |

A Problem Finance Teams and Sustainability Teams Both Know Too Well

Most organisations manage financial and ESG disclosure in separate workflows — different teams, different tools, different timelines. Both face the same structural failure when auditors arrive: evidence not captured at the time of reporting is extraordinarily difficult to reconstruct afterward.

On the Financial Reporting Side

The income statement closes, the financial statements go out, and then the audit begins. A late-stage adjustment to a revenue or cost figure was referenced in the management commentary, the strategic report, and the notes to the accounts — but only two of those three sections were updated when the number changed. The inconsistency surfaces during the audit.

Journal entries posted close to year-end often carry insufficient authorisation documentation. Consolidation adjustments and intercompany eliminations leave unclear evidence trails. The management commentary describes a margin improvement that does not reconcile cleanly with the financial accounts. For companies filing in ESEF-compliant iXBRL format, tagging completed after the narrative was finalised can leave disclosed values out of sync with the filed document if figures are subsequently revised.

Under PCAOB AS2810 and ISA 315, auditors must obtain sufficient appropriate audit evidence for all material figures and disclosures. Where contemporaneous documentation for significant entries or disclosure decisions is missing, additional substantive procedures are required — extending timelines and increasing cost for both sides.

The burden compounds at scale. For organisations managing hundreds of disclosure data points across financial and ESG domains, the difference between well-evidenced and poorly-evidenced workflows is measured in close days, audit queries, and restatement risk.

On the ESG Reporting Side

The sustainability statement is published, the CSRD submission is made, and then the assurance engagement begins. The practitioner requests the source data behind the Scope 1 GHG figure — and the team discovers that the utility invoices were filed separately from the emissions calculation, the emission factors were updated mid-year without documentation, and the person who made the methodology decision has since left the organisation.

Board approval of the sustainability statement may exist in email form but was never formally recorded against the disclosure. An ESRS datapoint for employee health and safety references a figure from the HR system, but the extract was taken at a date that does not align with the reporting period end. Year-over-year boundary definitions for the GHG inventory changed without a restatement note. Each of these gaps collectively constitutes a failure of the evidence chain that CSRD assurance requirements are designed to test.

According to ICAEW’s guidance on CSRD sustainability assurance, limited assurance practitioners will examine the materiality assessment process, test ESRS compliance, and verify that disclosures are not materially misstated. The quality of the evidence going into that engagement directly affects both the cost and the outcome.

Figure 1: Post-cycle evidence assembly vs. continuous evidence capture — the structural difference

The Regulatory Stakes — Converging on Both Sides

For years, financial and ESG reporting operated under different assurance regimes — financial statements under well-established audit standards, sustainability disclosures under voluntary frameworks with no formal verification requirement. That divergence is closing rapidly.

| Financial Reporting | ESG Reporting |

|---|---|

| PCAOB and ISA-based audit evidence requirements: Under PCAOB auditing standards and ISA-based audit frameworks, auditors are required to obtain sufficient appropriate audit evidence for material figures and disclosures.

ESEF / iXBRL (EU): Tagged financial statements must be consistent with the filed narrative document. Tagging errors and value mismatches are a compliance risk reviewed during audit. IFRS disclosure checklist compliance: Notes to accounts, segment reporting, and related party disclosures must each be supported by authorised source documentation. SOX 302/404 (SEC-registered companies only): Management must assess and document the effectiveness of disclosure controls and internal controls over financial reporting. |

CSRD under the revised Omnibus Directive (EU) 2026/470: Limited assurance is mandatory from the first year of application for in-scope companies (>1,000 employees and >€450M revenue under the revised Omnibus thresholds).

EU-wide limited assurance standards: To be adopted by the European Commission no later than 1 July 2027 under the Omnibus Directive framework. The Omnibus revisions have deprioritised the earlier progression toward mandatory reasonable assurance. ESRS data requirements: Each datapoint must be traceable to a governed source, with methodology documented and boundary definitions consistent year-on-year. ISSB / IFRS S1 & S2: Jurisdictions adopting ISSB standards expect sustainability disclosures to align with financial reporting timelines and governance frameworks. |

The direction across both regimes is the same: more evidence, more structured, more contemporaneous. As Compliance Week notes, reports can appear compliant with frameworks and deadlines while still lacking the traceable, evidence-backed documentation needed to support effective audit and assurance processes.

The convergence point is the annual report. Under CSRD, the sustainability statement sits inside the management report. Under ESEF, the financial statements are filed in Inline XBRL format. Under ISSB-aligned frameworks, climate disclosures are expected to align with financial reporting timelines. Two teams, two evidence challenges — increasingly converging within a single reporting and assurance environment.

What “Audit-Ready” Actually Means — For Both Teams

Audit readiness is widely misunderstood as a documentation exercise: gather the right files before auditors arrive. For financial reporting teams and ESG teams alike, that framing is what produces post-cycle scrambles.

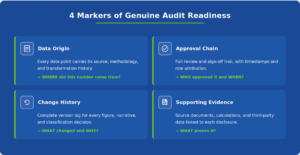

True audit readiness is a state, not a task. It means that at any point during or after the reporting cycle, any disclosed figure — whether a revenue line or a carbon intensity metric — can satisfy four tests with minimal reconstruction effort:

Figure 2: The four markers of genuine audit readiness — applied to financial and ESG disclosures equally

| Financial: Applied in Practice | ESG: Applied in Practice |

|---|---|

| Data Origin: Trace a revenue figure from the ERP transaction through consolidation to the income statement line and, where applicable, the iXBRL tag.

Approval Chain: CFO sign-off on financial statements, audit committee approval of significant accounting estimates — all formally recorded with timestamps. Change History: Every revision to a balance sheet figure, disclosure note, or management commentary paragraph, with the reason documented at the time. Supporting Evidence: Journal entry authorisations, bank reconciliations, board minutes — linked to the disclosure they support. |

Data Origin: Trace a Scope 2 figure from the utility invoice through the emission factor applied to the ESRS E1 datapoint in the sustainability statement.

Approval Chain: Board or committee approval of the sustainability statement, formally recorded — not captured only in email threads. Change History: Every revision to an emissions boundary, methodology note, or ESRS disclosure, with the rationale documented. Supporting Evidence: Utility invoices, HR system extracts, supplier certificates — stored alongside the calculations they support. |

Building audit-ready financial and ESG reporting workflows that satisfy all four tests requires the same architectural response from both teams — and ideally, the same platform delivering it.

Five Pillars of an Audit-Ready Reporting Workflow

Building audit-ready financial and ESG reporting workflows requires more than documentation. It requires a structured framework that supports evidence, governance, traceability, and approvals throughout the reporting cycle.

The five pillars below apply across both reporting domains. The mechanism is the same — only the data differs. Organisations that build all five into a single, unified workflow reduce audit risk on both sides simultaneously.

Figure 3: Five pillars of an audit-ready financial and ESG reporting workflow

1. Continuous Evidence Capture — Not Year-End Collection

Evidence should be attached to data points at the moment they are created. For financial teams, this means linking journal entry authorisations to the entries themselves, attaching bank reconciliations to balance sheet positions as they are finalised, and recording board minutes against the provisions and estimates they authorise — not filing them separately to be retrieved under audit pressure.

For ESG teams, it means uploading utility invoices alongside Scope 1 and 2 calculations as those calculations are built, storing supplier certificates with the Scope 3 data they support, and attaching committee minutes to governance disclosures the moment they are recorded. Evidence collected in real time reduces the volume of additional procedures auditors must perform. Evidence collected under deadline pressure raises questions that take time and cost to answer.

Auditors on both sides need to trace any disclosed figure back through every stage of its journey. For financial reporting, that means tracing a revenue figure from the ERP source transaction through consolidation, management review, and narrative references to the value in the filed document. For ESG reporting, it means tracing a carbon intensity metric from a raw utility bill through the emission factor applied, the calculation performed, and the ESRS datapoint disclosed.

Without this lineage, a single challenge to any figure — financial or ESG — requires teams to reconcile data across multiple systems and reporting periods. The principle of a traceable supply chain for each data point applies equally to a balance sheet estimate and a Scope 3 emissions figure.

Every material disclosure — a balance sheet estimate or a Scope 3 boundary definition — should pass through a defined approval workflow and leave a verifiable record. For financial teams, that means documented CFO and audit committee sign-off on significant accounting judgements with timestamps that align with the filing timeline. For ESG teams, it means board-level approval of the sustainability statement formally recorded against the disclosure, not captured only in inbox threads.

For integrated financial and ESG reporting, this matters on both sides simultaneously. When the same underlying data — a capital expenditure figure, for instance — flows into both the financial statements and the ESRS E1 climate disclosure, auditors check for consistency across both. A shared governed workflow reduces that consistency risk significantly.

4. Version Control and Full Change History

Every change to a reported figure or narrative — and the reason for it — should be captured automatically: revisions to income statement lines and balance sheet estimates for financial teams; methodology changes, boundary revisions, and restatements with documented rationale for ESG teams. The finance function’s existing discipline around accounting controls must now extend fully to sustainability data — and version history is the mechanism that makes that extension auditable.

5. Unified Financial and ESG Data in One Governed System

The fifth pillar is what makes the others sustainable at scale. When financial disclosure management and ESG disclosure management run in separate systems, the seams between them become audit vulnerabilities. A capital expenditure figure cited in both the financial statements and an ESRS E1 climate disclosure must be consistent. When two systems govern these numbers, that consistency depends on manual reconciliation under pressure. A unified platform embeds that consistency into the workflow itself.

How EcoActive Addresses Both

EcoActive is an AI-native unified financial and ESG disclosure management platform — designed around unified disclosure governance for financial and sustainability reporting. Where legacy tools treat financial and sustainability disclosure independently, EcoActive manages both in a single governed environment, capturing traceability, approvals, and supporting evidence continuously throughout the reporting cycle.

Figure 4: EcoActive — audit readiness built into every step of the financial and ESG disclosure workflow

Traceability by design — for financial and ESG data alike.

Every data point carries its lineage with it. Source documents, calculation methodologies, and transformation logic are linked directly to the disclosure they support. Auditors can trace figures back to their origin with significantly reduced manual reconstruction.

Approval workflows embedded in the process — for both teams.

CFO sign-off on financial statements and board approval of the sustainability statement are both captured through the same timestamped, role-based workflow. Every approval creates a defensible record that meets the documentation standards of financial auditors and CSRD assurance practitioners.

Continuous version control — across financial and ESG disclosures.

Every revision to a balance sheet estimate, a management commentary paragraph, or an ESRS datapoint is captured with attribution and timestamp. When an auditor asks why a figure changed between draft and final submission, the answer is immediately available.

Financial and ESG in one governed system.

Capital expenditure figures that flow into both the financial statements and the ESRS E1 climate disclosure are governed through a shared workflow, reducing reliance on manual reconciliation.

Explore how EcoActive supports financial close-to-report workflows, CSRD compliance, ESEF and iXBRL reporting, and integrated financial and ESG disclosure from one platform.

The Cost of Waiting Is Rising — On Both Sides

The assumption that audit readiness is a future state — something to build toward when assurance requirements formally kick in — is proving costly for finance and sustainability teams alike. Financial audit standards are not becoming less demanding. CSRD limited assurance is now mandatory for in-scope companies, with EU-wide assurance standards to be adopted by July 2027. And the annual report is increasingly one document, not two.

of organisations surveyed cite complex reporting requirements as a major obstacle

Source: 2025 Big Four ESG and financial reporting maturity research

The workflow practices described in this guide are not only relevant for large enterprises currently under mandatory assurance. Mid-market companies approaching CSRD thresholds — or beginning voluntary sustainability reporting alongside their financial disclosure — benefit from building evidence capture, approval workflows, and data lineage into their reporting processes now. The architecture required for a limited assurance engagement is the same whether you build it under deadline pressure at the point of obligation, or by design in the reporting cycles before it. The difference is cost, risk, and disruption. Audit-ready workflows are a sound investment at any stage of assurance maturity.

The organisations that navigate this transition most successfully are those already treating audit readiness as a fundamental property of how they report — not a compliance project layered on top of an existing workflow.

That shift starts with choosing a disclosure management platform that captures evidence as reporting happens — for financial data and ESG data equally. Because by the time the audit begins, the only question that should remain is where to send the files — not where to find them.

Ready to make your financial and ESG disclosure workflow audit-ready from day one?

Visit ecoactivetech.com to see how EcoActive brings Financial and ESG audit readiness into one governed platform.